Are you a homeowner considering refinancing your FHA-insured mortgage? If so, the FHA Streamline Refinance program might be an excellent option, offering a simplified process and potential financial benefits by lowering your interest rate and monthly payments.

What is a FHA streamline refinance?

Introduced by the Federal Housing Administration (FHA), this program allows borrowers to streamline the refinancing process, reducing paperwork and saving time and money.

The FHA Streamline Refinance program is designed to help homeowners with existing FHA-insured mortgages take advantage of lower interest rates without going through a lengthy and complex refinancing process. The program’s primary objective is to make refinancing more accessible and affordable for borrowers who wish to lower their FHA streamline refinance rates and monthly mortgage payments.

Key Features of the FHA Streamline Refinance Program

- Fast and Easy: This program streamlines the process by not requiring a new property appraisal. This allows refinancing even if your home value has decreased or your financial situation has changed slightly. Because you skip the appraisal, there is no cost and no hoops to jump through regarding the appraisal process.

- Limited or No Verification of Income or Employment: Unlike when you first qualified for your FHA Loan, the Streamline refinance does not require verifying your income or employment. This saves time and paperwork and also makes it easier to qualify.

- Lower Closing Costs: The program aims to reduce upfront costs by allowing borrowers to finance the upfront mortgage insurance premium and other closing costs, minimizing out-of-pocket expenses. You may also receive a partial refund of the new upfront mortgage insurance premium.

- Lower Monthly Payments: By refinancing through the FHA Streamline program, homeowners can reduce their monthly mortgage payments by taking advantage of lower interest rates.

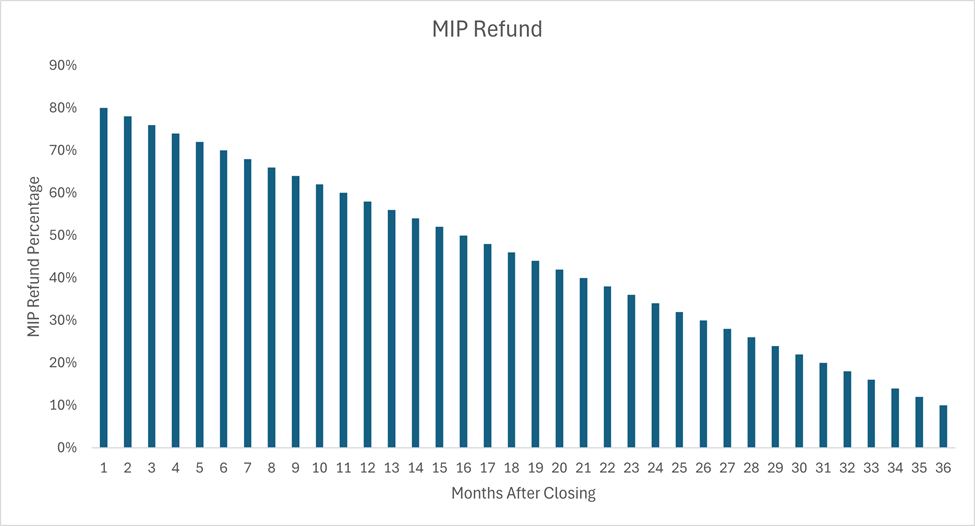

- Lower MIP Rates and Refunds: Homeowners who use the FHA Streamline Refinance may be refunded up to 68% of their prepaid mortgage insurance (UFMIP), which will be applied as a credit towards the UFMIP on the new loan.

- No Full Credit Check: A low credit score won’t stop you from using this program’s non-credit qualifying option, which is uncommon in other refinance loans. We must check your mortgage payment history, not your credit score.

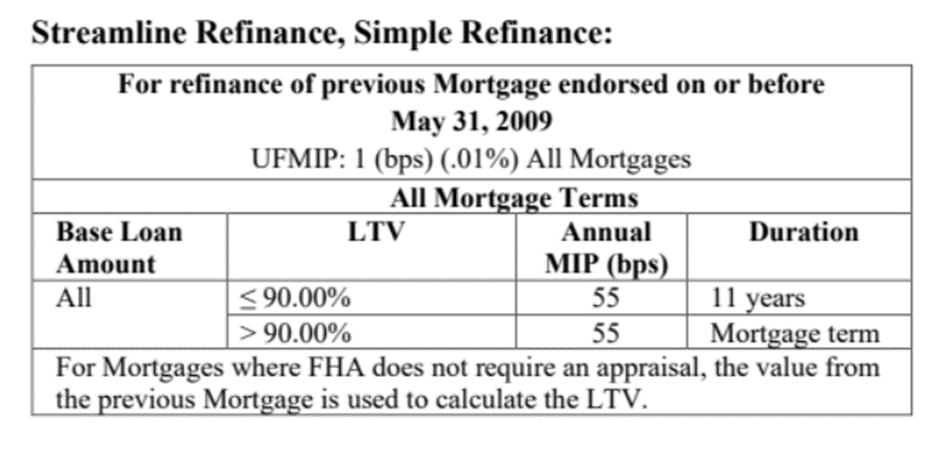

- Reduced Monthly Mortgage Insurance (MIP) payments in March, 2023: On March 20, 2023 FHA reduced the MIP rates for FHA Streamline Refinances from .85bps to .55bps

This savings is not retroactive, meaning, the MIP on your current FHA loan will not automatically drop. The MIP reduction is only available to new FHA Loans. If you do choose the FHA Streamline, Simple Refinance program, your new MIP will be .55bps.

Here is a practical example:

Current Loan Balance: $100,000

MIP Payment at .85bps: $70.83 / month MIP Payment at .55bps 45.83 / month

Streamline Your Savings: Navigating FHA Refinance Requirements

The FHA Streamline Refinance program offers a simplified path to lower your monthly mortgage payment and interest rate. While it streamlines the process compared to traditional refinances, specific eligibility requirements must be met. Let’s explore the key FHA streamline refinance guidelines and navigate the path toward potential savings.

Essential Requirements for Streamlined Savings:

- Maintaining a Good Payment History: The FHA prioritizes responsible borrowing habits. To qualify, you must have had no more than one 30-day late payment for all mortgages on the property for the previous six months. While one late payment within the last year may be permissible, your loan must be current at closing.

- Meeting the 210-Day Seasoning Threshold: Patience is vital. The FHA requires a minimum of 210 days to have elapsed since:

- The original purchase of your home, or

- The closing date of your last refinance on the same property.

FHA is concerned about early re-payment of their loans and this waiting period demonstrates your commitment to your current mortgage before pursuing a refinance.

- Demonstrating a Clear Financial Benefit: The FHA doesn’t approve refinances solely for convenience. You must show a “Net Tangible Benefit” from the refinance. In simpler terms, the new loan must offer a tangible financial advantage compared to your current mortgage.

Here are two ways to achieve a Net Tangible Benefit:

- Reduce your combined interest rate: This is typically achieved by securing a lower interest rate on your new loan. Aim for a combined reduction (interest rate + mortgage insurance premium) of at least 0.50% compared to your current combined rate.

- Switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage: This provides predictable monthly payments and reduces the risk of future rate fluctuations, potentially saving you money in the long run.

Important Note: Taking cash out of your home equity is prohibited with a Streamline Refinance. However, the FHA offers a separate cash-out refinance program if this is your goal.

Beyond the Basics: Additional Considerations

While these are the core requirements, it’s crucial to remember that not all lenders strictly adhere to the FHA’s minimum guidelines. Some lenders might have stricter requirements, such as minimum credit score thresholds.

Shop Around and Seek Guidance: If your current lender requires additional documentation beyond the FHA’s minimums (like a home appraisal or income verification), don’t hesitate to explore other lenders who adhere to the official FHA Refinance guidelines. It’s also wise to consult a qualified mortgage professional who can guide you through the process, assess your eligibility, and help you find the best loan terms.

By understanding these requirements and exploring your options, you can leverage the FHA Streamline Refinance program to streamline your savings and achieve your financial goals.

To qualify for the FHA Streamline Refinance program in 2024, you must meet the following requirements:

- Have an existing FHA-insured mortgage.

- Be current on your mortgage payments (with some exceptions).

- The refinance must have a net tangible benefit, such as lower monthly payments.

- Have owned the property for at least six months.

- You can have up to one FHA Streamline loan at a time.

Maximizing Your Advantage: The FHA UFMIP Refund and Streamline Refinancing

When you initially obtain an FHA loan, you pay an upfront mortgage insurance premium (UFMIP) for closing costs. This premium helps protect the lender if you default on your loan. However, suppose you refinance your FHA loan through a streamlined refinance within the first three years of your original loan. In that case, you may be eligible for a partial refund of your UFMIP.

The amount of the refund you receive depends on how long you’ve held your original FHA loan:

- Within the first year, You can receive up to 68% of your original UFMIP.

- After one year, The refund percentage gradually decreases.

This refund is not issued as cash but instead applied as a credit towards the UFMIP you would pay on your new FHA loan. This can significantly reduce your upfront costs when refinancing and provide additional funds for other purposes.

Conclusion

With its potential UFMIP refund benefit, the FHA Streamline Refinance program continues to be an attractive option for homeowners in 2024—understanding FHA Streamline Refinance pros and cons will help you make better decisions. It provides a streamlined process, lowers documentation requirements, and reduces upfront costs, making it easier and more affordable for homeowners to refinance their FHA-insured mortgages. Before making a decision, it’s crucial to consult with a mortgage professional who can guide you through the process and help you determine if this program is suitable for your specific needs.